Projects

Work in progress

The Macroeconomics of Energy Security: Anatomy of a Multi-Frequency Index

with Julian Marcoux (University of Lausanne and PhD Globalization fellow Dartmouth College)

Safe-Haven Effects and Sectoral Implications: Lessons from Switzerland and Japan

with Mathieu Grobéty (CREA)

Master Thesis

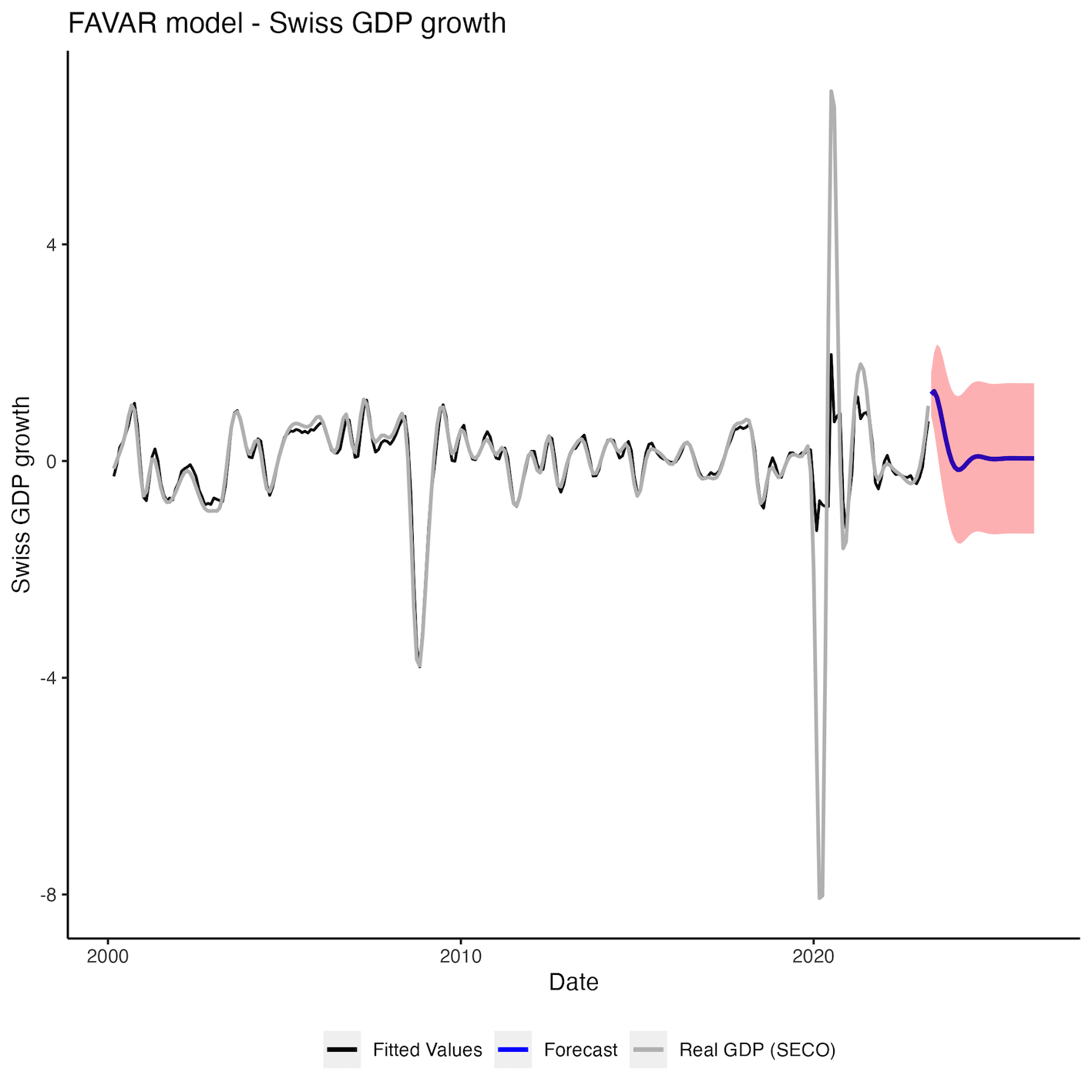

Forecasting the Swiss Economy - FAVAR approach

under the supervision of Mathieu Grobéty (head of CREA) and Brendan Berthold (Zurich Insurance)

Abstract:

Conducted for CREA (Swiss Institute of Applied Economics of University of Lausanne), we propose a Factor Augmented VAR (FAVAR) tailored for a small economy to forecast real Swiss GDP growth. We use principal components analysis and expectation-Maximization algorithm to extract factors from a diverse set of a large number of variables with missing values and modeled them with the target variable within a VAR framework in a two step estimation approach. Our FAVAR remains structural by dividing the model into two blocks : one for foreign and one for domestic factors. Each block encompasses a real activity, inflation, money supply & interest rates and financial conditions factor, contributing to the model’s economic interpretability. To assess its out-of-sample performance, we compare our FAVAR model against six different benchmarks, including univariate and multivariate models, across various forecasting horizons (up to 12 quarters ahead) and over three different evaluation samples. Our key finding suggests that the performance of the FAVAR increases with the forecasting horizon. However, the Covid-19 crisis and the war in Ukraine present challenges to our FAVAR’s performance. During this period (2020Q1-2023Q2), we found a decline in forecast performance over the long term as well as a general deterioration across all horizons except when compared to the random walk.

Genève est-il un canton attractif ? Une analyse économique sous l’angle de cinq thématiques (Policy)

Résumé | Rapport

| Communiqué de presse

avec Mathieu Grobéty (CREA)

Présentation:

Cette étude, mandatée par la Fondation de l’attractivité du Canton de Genève et à laquelle j’ai contribué avec Mathieu Grobéty (directeur exécutif du CREA) en avril 2023, analyse l’attractivité du canton de Genève sous l’angle des finances publiques, de la fiscalité, de l’innovation, de la durabilité et des infrastructures. L’attractivité du canton est mesurée par un grand nombre d’indicateurs économiques ainsi qu’à l’aide de nos outils macroéconométriques, et est comparée à ses concurrents directs à l’échelle nationale (Vaud, Zoug, Zurich et Bâle).

Unpublished works

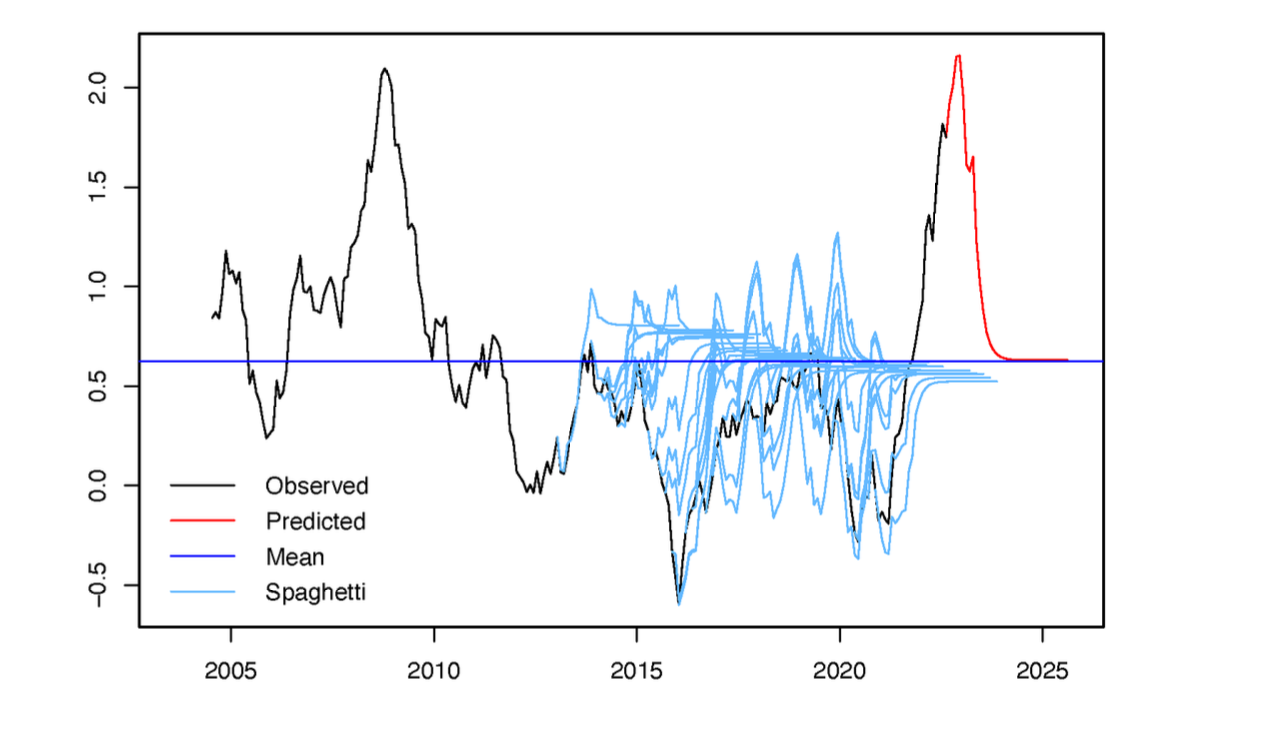

Forecasting Swiss CPI (term paper)

with Mora Klimberg (IATA) and Pasha Mammadov (International Federation of Red Cross)

Abstract:

This paper explains how to forecast monthly Swiss CPI Inflation for the next 3 years from October 2022 using disaggregated CPI components : ARDL modeling European imported inflation since the EU is one of the key partners of Switzerland, ARMA modeling domestic inflation and ECM capturing only oil products volatile part. Then, we aggregate all these three CPI components into one combined model taking into account their past respective weights over time. Finally, we assess the out-of-sample performance of our combined model. It does not beat the AR(1) benchmark over short horizons (up to 3 months) but performs relatively well over the long term even if our combined model is statistically similar to the benchmark over most horizons.

Analysis of an impact of monetary shocks through policy rate on two european eastern economies (term paper)

with Lisa Wenger (Swiss National Bank) and Dario Vacchini (ETH Zurich)

Abstract:

In this paper we investigate the impact of monetary shocks in two Eastern European economies: Romania and Slovakia. We implement two structural VAR models to analyze the effect of the policy rate of the respective country on three economic variables: GDP growth rate, inflation and EUR/USD exchange rate. In Romania, we find that GDP growth reacts negatively to monetary shocks, while in Slovakia the response is oddly positive even though not significant. The reaction to inflation is negative for both countries and more pronounced for Romania. Thus, the integration in Eurozone of Slovakia could dampen the magnitude of its shocks.